Insurance plays an important role in how quickly people, businesses, and governments recover after natural catastrophes. Unlike indemnity policies, which rely on a potentially lengthy claims process, parametric policies trigger rapid payouts based on the physical characteristics of an event and can be used towards a broad range of losses. For these reasons, parametric policies may be used as a complement to indemnity insurance to disburse funds in a fast and transparent manner. Since they are not linked to specific losses sustained by a given physical asset, they have been used successfully by governments to cover emergency and response costs and by corporations to cover business interruption losses. They can be structured as insurance, reinsurance, derivatives, catastrophe bonds, and other financial vehicles, depending on the regulatory environment.

Parametric insurance solutions are often subject to basis risk, the misalignment between sustained losses and monetary recovery. For this reason, they need to be critically evaluated, assessed, and understood when considering them in risk management strategies. GC StormGrid and GC FireCell are Guy Carpenter proprietary engines to design high-resolution parametric tropical cyclone and wildfire solutions. GC parametric solutions minimize basis risk, are well suited to design parametric transactions for spread-out portfolios of exposures, and are available globally. Examples for each of these products are presented below.

GC StormGrid

GC StormGrid is used to design parametric tropical cyclone covers that respond to track information published in real-time by global meteorological agencies. GC StormGrid uses a cat-in-a-grid trigger, building on the concept of a cat-in-a-box, which has a long history in the market and triggers a payout if an event’s intensity (e.g., sustained wind speed) exceeds a threshold within a geographic domain. Cat-in-a-grid designs consider a grid of cells instead of a single geographic domain, which limits the potential of missing events and reduces basis risk. To illustrate the design and trigger of a GC StormGrid solution, we present a cover created for Florida and show how it would have triggered during Hurricane Ian (2022).

The presented parametric cover for Florida consists of over 200 cells, each calibrated using the results of a catastrophe model to produce a loss estimate to the state’s industry exposure. When Hurricane Ian passed from southwest to northeast across the Florida Peninsula, it crossed 19 cells included in the transaction and reached maximum wind speeds of a Category 4 hurricane. GC StormGrid monitored the progression of the track, using the reported positions and sustained wind speeds to calculate a parametric loss estimate. This was sufficient to reach the attachment level of the parametric structure and would have resulted in a payout.

Exhibit 1

Top: Track progression map for historical event Ian (2022) with color proportional to reported sustained wind speed; Center: Maximum wind speed along track with GC StormGrid cells shown in red. Shades are proportional to the quality of each cell’s loss model; Bottom: Loss computed according to the combination of the individual cell estimates. Final estimate exceeds the attachment level of the parametric structure, shown as horizontal gray line, and would have triggered a payout.

GC FireCell

GC FireCell is used to design parametric wildfire covers indexed to wildfire data published in real-time through NASA’s Fire Information for Resource Management System (FIRMS). Based on the evidence that damage to a specific asset tends to be binary depending on whether the wildfire has reached that asset or not, GC FireCell produces a recovery if a wildfire event is detected within the asset’s proximity. Specifically, the design discretizes an area that includes the insurable assets into a high-resolution grid of virtual stations. A limit value proportional to the total insured value is assigned to each virtual station. A payout is triggered when a fire observation from the MODIS or VIIRS satellites, made available by FIRMS, overlaps any of the virtual stations. If a virtual station is activated, its associated limit is disbursed.

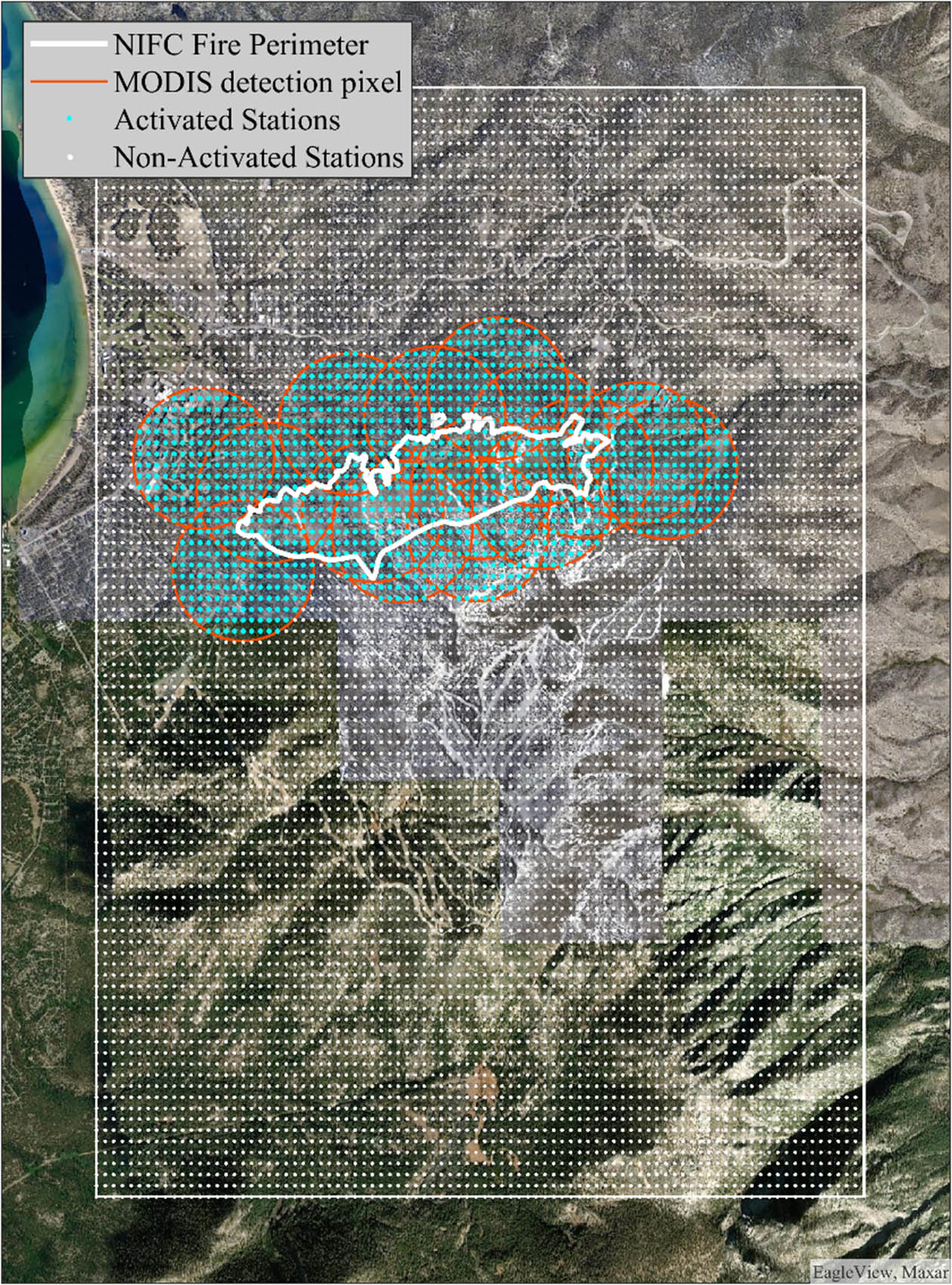

To illustrate this process, we present a cover created for a region in the United States and show how it would have triggered during the Gondola Fire (2002). The parametric cover was calibrated to respond to loss-causing events in South Tahoe, California and consisted of 8,900 virtual stations regularly distributed across the coverage area. On July 3, 2002, the Gondola Fire started and proceeded to burn more than 600 acres and threaten more than 550 structures. FIRMS produced fifteen satellite fire observations for this event. Ultimately, 1,272 of the 8,900 virtual stations fell within the footprint of the fire observations and would have triggered a payout equal to the sum of the limits at the activated stations (see Exhibit 2).

Exhibit 2

The coverage area (shown as a white rectangle) near South Tahoe, California was discretized into a regular grid of virtual stations (shown as points). During the Gondola Fire (2002) FIRMS reported fifteen fire observations (footprints outlined in red). The fire observations activated any virtual station within these footprints (shown in blue).