This article was first published by Oliver Wyman here.

Australia’s largest banks have signed up to the Net Zero Banking Alliance (NZBA). The NZBA requires the banks to publicly announce within three years the interim carbon emission targets that they will aim to meet by 2030. These targets are designed to be consistent with the global carbon budget required to achieve a 1.5 degree temperature increase globally within the century, requiring net zero emission by 2050. The targets that have been announced are ambitious, as a 1.5 degree scenario requires rapid action to be carried out in the power and resources sectors before 2030, with other sectors like transportation, manufacturing, agriculture and land use to follow soon afterwards. Residential and commercial real estate will also be required to make large reductions in emissions.

Setting the targets has been the first step and is comparatively easy; operationalization of activities to achieve them is much harder and comes next.

Operationalization of activities to meet emissions targets will require banks to develop a number of new capabilities:

- New measurement: Banks are required to measure the emissions footprint of their own operations and more importantly, their financed emissions. This will include the banks’ customers’ scope 1 and 2 emissions – and where material, scope 31 emissions (most important for coal mining, oil & gas extraction, auto manufacturing, and construction). At this point in time, Australian banks’ current measurement methods still rely heavily on averages and estimates.

- New reporting: Banks will be required to report annually on their emissions footprint, its evolution and the activities they are undertaking to reduce it.

- New decision making and portfolio steering: Banks will be expected to make decisions on individual lending or investment decisions based on their expected impact on their emissions profile and transition pathway, balancing these alongside other strategy, risk, and return considerations.

- New supporting operating models: Banks will need new data, systems, processes, people, and governance structures to do all the above effectively.

Description of Scope 1–3 emission types

Department of climate change, energy, the environment and water

Source: National greenhouse accounts

When it comes to measuring hot air, it’s hard to know which house is better

Measurement and reporting on the emissions profile of the banks will be a huge challenge, and one which banks are just starting to turn their attention to. Some have likened its scale to the 2004 Basel II regulations which forced banks to implement a materially more sophisticated and data intensive approach to credit decisioning and reporting. In the future, assessment of carbon exposure on any lending decision will need to go hand in hand with credit risk, fraud and anti-money laundering assessments.

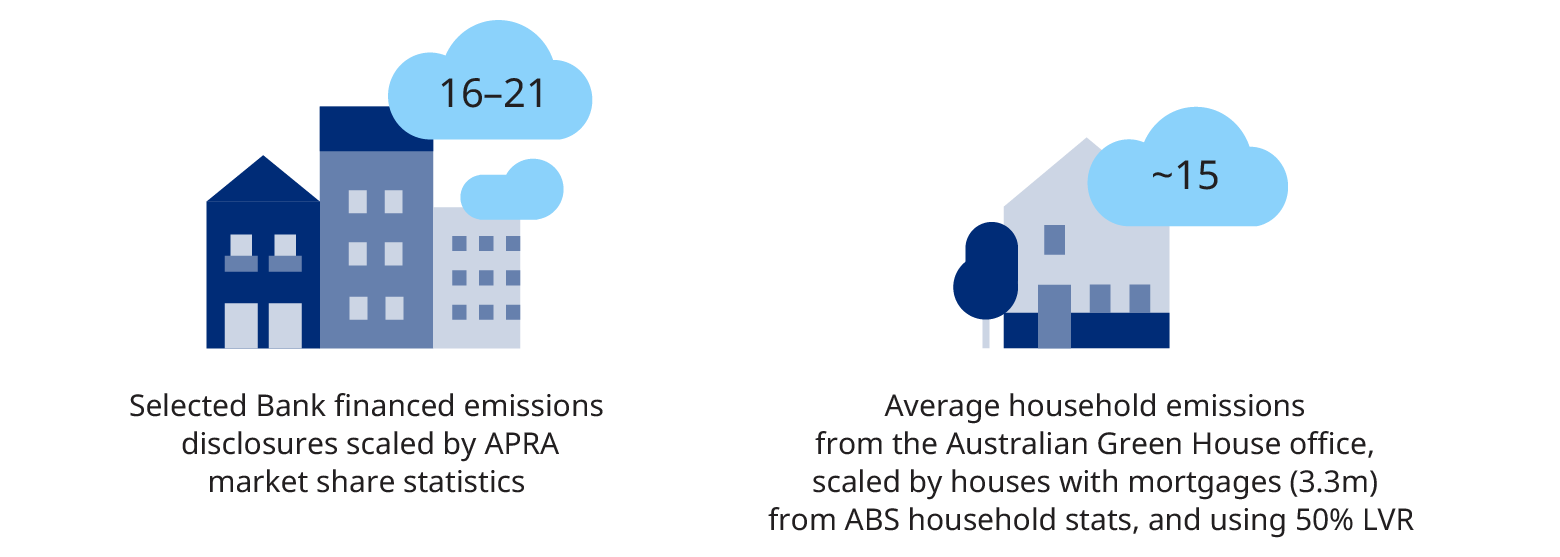

Mortgages represent a particularly large challenge. At this point in Australia the only public information that can be used to estimate the emissions intensity of a property is the property type, size, and age of its construction. This is in contrast to the UK and Europe where banks are given access to a database of Energy Performance Certificate (EPC) ratings that can be mapped to any property. These allow them to identify and attribute meaningful differences in energy efficiency across their property portfolios. As the same information does not exist in Australia, banks here are forced to use foreign emissions factors in their own estimation methodologies for domestic emissions, with the acknowledgement that the data accuracy of the resulting figures is likely to be low.

We see a wide range of estimates for the aggregate financed emissions of Australian mortgages within bank portfolios, ranging from 10 – 21 Mega tonnes of CO2 equivalent. Such a wide range is not surprising given the lack of accurate data available at this point, however regardless of where in the range the actual emissions amount may be, they are still a highly material emissions problem.

Estimating aggregate mortgages financed emissions

Resulting emissions estimate (in Mega tonnes of CO2 equivalent)

Enter the Consumer Data Right, an unexpected solution

From November 2022, all major Australian energy retailers will be required to make their data available in Australia’s Open Data ecosystem, the Consumer Data Right (CDR) regime. The data provided into the regime will include detailed information on the energy consumption of individual households and commercial properties (electrical and gas) for up to two years. The regime was designed to give customers greater ownership and privacy rights on their information, foster faster provider switching, and accelerate product and service innovation. In this case however, it would also provide banks (that are regulated as Accredited Data Recipients in the regime) with a way to potentially source direct, accurate emissions data on the largest portfolio of assets on their balance sheet, and reduce reliance on averages and overseas emissions benchmark factors.

Adatree, a regulated technology provider of CDR access and consent management infrastructure, is ready to start testing energy data through the CDR eco-system for Open Energy use cases. They observe that there are energy Data Holders who have already passed conformance testing before the November 15 deadline, which is significantly ahead of where the banking sector was at the equivalent time. This bodes well for the pace at which energy data may be provided and consumed through the CDR eco-system relative to the introduction of banking data.

We believe that Energy CDR data is on track for a considerably smoother faster roll-out than we saw with banking data before.Alex Scriven, Chief Operating Officer, Adatree

Only the start of the solution

While the use of CDR data is promising, there is much work to be done around acquiring, using, storing and processing that data in a way that is consistent with regulations. To be successful, banks will have to develop new value propositions, balance achieving their goals with strict usage and privacy constraints, and develop the required technical infrastructure, supporting capabilities and partners to effectively consume and analyse the new data.

The opportunity for CDR energy data to greatly improve emissions reporting and management is clear, the size of the prize is material. It will be up to leading banks to design and deploy customer value propositions that will enable them to achieve it.