This perspective is based on the testimony to the United States House of Representatives Financial Services Committee, Subcommittee on Housing and Insurance given on behalf of Marsh McLennan by Julian Enoizi, Head of Public Sector at Guy Carpenter. The hearing, titled Encouraging Greater Flood Insurance Coverage in America took place on March 10, 2023.

The flood protection gap

Despite being one of the most common and destructive natural hazards, flood risk is systematically underestimated, which contributes to inadequate insurance, underinvestment in flood resilience, and policy decisions that, in many cases, may not be helping.

Coupled with increased urbanization, economic development and population growth, more frequent and intense flood events are putting a greater proportion of people and infrastructure at risk. According to the Marsh McLennan Flood Risk Index, 18% of the global population is currently threatened by flooding, a number projected to rise considerably in the coming years.

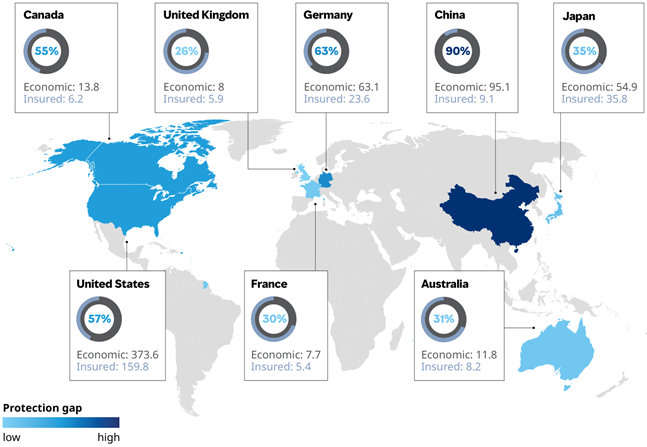

As exposure to flood risk increases, so does economic damage, of which only a small proportion — 12% worldwide since 1980 — has been insured. In inflation-adjusted 2021 dollars, global economic losses from floods increased from $504 billion in the 15-year period between 1992 and 2006 to $729 billion between 2007 and 2021. Among the costs, business interruption damages often approach or exceed those of physical damages as global supply chains expose business activities to floods thousands of miles away. Comparing economic and insured losses from the last decade reveals the significant insurance protection gaps existing in many countries (see Exhibit 1). Gaps in flood risk protection exist not only in insurance coverage, but in resilience measures that can help communities minimize and recover from losses.

Both insurers and policyholders felt the impact of increased flood losses and other disasters during the particularly challenging insurance program renewals on January 1, 2023. According to Marsh’s Global Insurance Market Index, property insurance pricing increased by an average of 11% in the US and 7% globally in the fourth quarter of 2022 alone.

In 2022, flooding was the dominant contributor to global losses that were estimated at $270 billion, of which approximately $120 billion were insured. A snapshot of 2022 flood-related losses includes:

Hurricane Ian, the third costliest weather disaster on record, killed more than 160 people and caused $100 billion in losses, $60 billion of which was insured, on its path from the Caribbean and up the US coast from Florida through the Carolinas.

Hurricane Fiona dumped 30 inches of rain in Puerto Rico, causing widespread power outages, multiple deaths, and billions in losses. The Federal Emergency Management Agency (FEMA) has provided over $700 million in federal grants to the government of Puerto Rico and to households. However, few Puerto Rican households have flood insurance, with only $2.7 million in claims for flood damage related to Hurricane Fiona.

In eastern Kentucky, historic summer flooding caused at least 37 deaths and more than $1 billion in damages. It’s estimated that less than 3% of affected properties were covered by flood insurance.

Floods in Pakistan caused an estimated 1,700+ deaths and $15 billion in damage, almost none of which was insured.

In Australia, floods caused $8.1 billion in damages, about $4.7 billion of it insured.

In the first few months of 2023, historic flooding continues. In New Zealand, flooding in January and February resulted in tens of thousands of insurance claims. Current estimates by the NZ government say losses are expected to top $8 billion.

Flood risk financing exists in many developed countries, with the predominant model a government-backed program, such as the NFIP. In many countries, standalone flood insurance from either public or private sources is limited.

Exhibit 1: Map showing cumulative flood losses ($ billions) and protection gaps across select countries between 2012 and 2021

Note: Economic and insured loss data for the United States includes tropical cyclones; data for China and Japan includes floods and tropical cyclones; data for France, Germany, and Canada includes floods and severe convective storms; data for Australia includes floods, tropical cyclones, and severe convective storms. Data: Swiss Re.

Source: Staying above water: A systemic response to rising flood risk, Marsh McLennan, 2023.

Closing the protection gap

Flooding disproportionately affects lower income communities, which are more vulnerable and more exposed to flooding. One way to help bridge the divide is by increasing participation in flood insurance. Studies have shown that individuals and communities with flood insurance recover better and faster than those without. Insurance, however, is but one piece of a national flood resilience strategy, along with investment in flood protection and resilience, enhanced access to flood risk data, and effective land-use planning.

While insurance is a critical part of recovery from natural disasters, many households and businesses do not have adequate coverage for repairs and rebuilding. This is a scenario that has been playing out in recent months in the recovery efforts from Hurricane Ian, last summer’s devastating floods not limited to eastern Kentucky, and Missouri.

The reasons for low coverage rates vary, and include affordability constraints, limited risk awareness, poor understanding of insurance, and behavioral biases in decision making. The protection gap in the United States and elsewhere means that many individuals, businesses, and communities do not have the financial resources to effectively recover following a flood or another disaster.

The growing role of parametric insurance to in flood risk readiness and mitigation

As an alternative risk transfer solution that is growing in demand to improve climate resilience, parametric insurance deploys a measurable index with predefined triggers that can pay out once pre-determined conditions are met. Unlike most forms of traditional property insurance, pricing is based primarily on the probability of the loss indexed being triggered rather than the specific risk of damage suffered by the benefits recipients. This is particularly effective where it is either not possible, feasible, or desirable to assess the underlying exposed interests. Parametric solutions offer a more expedited contract payout, typically moving funds into the hands of those who have suffered loss in a matter of days, which can accelerate recovery. This is particularly important when it comes to floods, as a delay in restoration can result in proliferation of mold which contributes to health problems over time.

Community-based catastrophe insurance

Marsh McLennan has been a proponent of an innovative approach to boosting insurance purchasing known as community-based catastrophe insurance (CBCI). This provides disaster insurance arranged by a local government, quasi-governmental body, or community group to cover a group of properties. This type of program is flexible and can cover a single hazard or a range of natural disasters for a given community, including floods, wildfires, and earthquakes.

The benefits of CBCI fall into three main areas: enhancing financial resilience; providing affordable coverage; and creating incentives for risk reduction at the community and individual level (see Exhibit 2).

The costs of disasters are often deferred until they occur. However, with CBCI these costs can be quantified, enabling the community to invest in mitigation measures with the funds that would have been used for disaster recovery. This not only minimizes the impact of the disaster, but also fosters a culture of preparedness that has been shown to accelerate recovery. The funds made available through CBCI schemes can be used to “build back better”, thus minimizing future impacts. For flood risk, this could mean levee improvements and ecosystem-based interventions such as wetlands enhancements.

Such broad applications can further incentivize a community’s risk management efforts, including risk reduction, risk communication, and risk transfer. Communities that opt for community-based catastrophe insurance have a higher chance of recovering – and do it faster. They have better access to funding, which makes it possible to contain the negative consequences of disasters, including loss of GDP. For instance, a coastal community that depends on tourism can prepare for major storms in advance and take necessary measures to limit impacts, thus mitigating loss of revenue.

Exhibit 2: Potential benefits of CBCI

Source: Community-Based Catastrophe Insurance: A model for closing the disaster protection gap, Marsh McLennan, 2021.

CBCI offers great flexibility in its structure and design, with varying degrees of community responsibilities possible. These range from a facilitator model where the community members contract with insurers, all the way through to a captive insurer in which the community establishes and operates its own risk-bearing entity.

The design and deployment of CBCI programs can be facilitated by solutions utilizing parametric triggers, as these have the potential to attract additional capacity and involve less risk in terms of implementation compared to solutions requiring a more granular evaluation of exposures and losses.

A CBCI pilot program: Boosting financial resilience in NYC neighborhoods

One benefit of community-based catastrophe insurance is the flexibility it allows in defining “community”, which can be an agency or municipal government, a neighborhood association, a business improvement district, or any number of entities. The primary requirement is that the involved community has the authority to secure or facilitate insurance coverage on behalf of multiple properties.

Marsh McLennan is currently involved with a project in New York City, which will establish it as one of the first local governments in the United States to harness CBCI. The project’s goal is to increase the financial resilience of low- and moderate-income households to flood risk. These communities are increasingly vulnerable to flooding and are, in many instances, under or uninsured.

Guy Carpenter and MMC Securities, both units of Marsh McLennan, are working with the City of New York and the Center for NYC Neighborhoods (CNYCN) and others to pilot the program in designated neighborhoods. Many of the potential benefit recipients cannot afford flood insurance or are locked out of the traditional insurance market.

The program is built on a parametric insurance contract. Payouts will be made to CNYCN for qualifying flood events based on a mix of satellite data, on-the-ground real-time sensors, and social media images. Once a qualified event triggers the payment, homeowners will be able to apply for assistance — on their own or with help from CNYCN’s network partners. Qualified applicants can then receive a grant up to $15,000 from CNYCN within days of a major flood.

The intent of these payments is to support residents and their broader communities in getting back to normal faster. It also will allow them to avoid having to make such tough decisions as whether to pay for home flood repairs versus other critical family needs, like healthcare, food, and saving for education.

The kickstart of this innovative program can help other communities to establish their own CBCI program, possibly with federal grant funding acting as a catalyst.

Flood risk and the need for a disaster resilience strategy

Given the scale and complexity of the challenges presented by flood risks, society needs a clearer vision that moves beyond unsustainable paradigms of protection and strikes a balance between addressing crises and building resilience. Insurance and risk transfer have an important role to play, but must be combined with a broader, coordinated resilience strategy.

Ideally, insurance would be paired with risk reduction measures such as hazard mitigation, building codes, and community resilience planning. Pairing these measures with risk transfer solutions—such as parametric solutions and CBCI programs—can be a force multiplier.

CBCI and other private risk transfer programs could be more successful if disincentives present in existing statutes and regulations are addressed. Similarly, the insurance industry should work with FEMA and code-setting organizations, such as the International Code Council (ICC), to develop incentives that would encourage additional flood mitigation investments. For example, FEMA and the insurance industry could review ICC limits to encourage investments after a flood loss. And more broadly, other industries, such as finance and real estate, can incentive further flood resilience investments together with the insurance industry and government.

Leaving the flood protection gap unaddressed will compound its costs and the devastating impacts on individuals and communities. As highlighted in a recent report from Marsh McLennan — Staying Above Water: A Systemic Response to Rising Flood Risk — three ways forward present themselves for transforming flood risk management.

1. Learning to live with floods through a cross-societal push for resilience, with communities, businesses, and governments implementing small-scale measures to mitigate risks and minimize damage.

2. Building strategic protection by deploying large-scale systemic interventions to protect critical assets and ensure financial resilience.

3. Preparing for relocation by facilitating resettlements of people and assets from high-risk areas in a timely, equitable, and financially viable way.

Financing and implementing these strategies will require decisive action, effective leadership, and innovations such as those being tested now in community-based catastrophe insurance projects. Critical enablers across governance and risk culture, land use and infrastructure planning, and finance and insurance are necessary to turn the flood resilience vision into reality and close the protection gap.