This article was first published by BRINK here.

Businesses need to ignore the conflicting news and focus on the basics: employees, customers and scenario planning.

Just as we hoped the world would return to some semblance of normal, the conflict in Ukraine, pent-up demand and ongoing tremors from the pandemic have contributed to unprecedented inflation and more uncertainty.

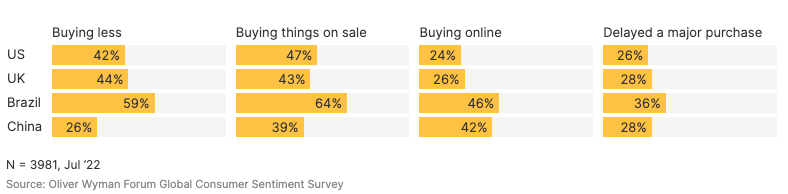

Businesses can’t afford to wait for stability. Higher food and energy prices already are impacting consumers, forcing them to change how they shop, save and work. More than 40% are buying less, and over a quarter are delaying major purchases, according to a monthly survey of consumers in the United States, the United Kingdom, China, and Brazil by the Oliver Wyman Forum.

And depending on what you read or whom you listen to, we’re headed either for a smooth landing or a turbulent ride. Companies must ignore the noise and focus on scenario planning, investing in talent and retaining their best customers to limit risk and unlock new opportunities.

Economic Uncertainty

Traditional rules don’t seem to apply to the current economic crisis. U.S. payroll employment, for example, returned this year to pre-COVID levels, but household savings dropped, credit card debt ballooned and the stock market experienced its worst first half since the 1970s.

Similarly, annual inflation hit a 40-year high in Britain while unemployment dropped to its lowest level since 1974, even as a record number of people were experiencing long-term illness.

Even China — the world’s second-largest economy and largest e-commerce market — has lost steam. The International Monetary Fund in May cut China’s expected GDP growth to 3.3%, which would be the slowest in four decades.

Until now, most companies have been able to shift higher costs onto consumers, but that won’t last. About a third of consumers in the United States and a quarter in the United Kingdom expect to spend even less in coming months, potentially impacting holiday sales and inventory levels.

Better Data and Planning

Companies need to be proactive with their strategies and prioritize scenario planning to navigate the volatility. They can begin by identifying potential threats, such as rising energy costs, supply chain disruptions, wage inflation and the ability to hire and retain talent. The second step is to develop worst-case, best-case, and middle-ground scenarios that could provide a road map and practical solutions no matter how bumpy the ride. Scenarios also are crucial in determining investment opportunities and untapped markets, as well as potential cost reductions.

Companies also need to analyze the composition of their workforces and customer bases to understand their needs, which likely changed during the pandemic. The data, while an added expense, could be used to determine pricing, product changes and how best to use existing talent. We’ve found in our surveys that segmented analysis often provides the details crucial to management. For example, while 77% of people were satisfied with work, a deeper dive showed a significant younger cohort was dissatisfied.

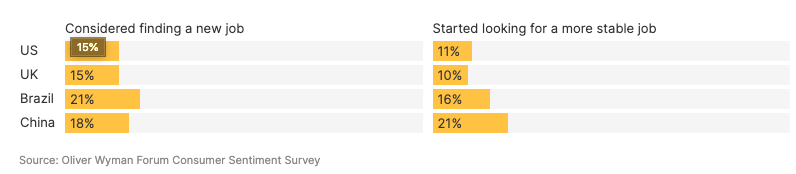

At the same time almost three-quarters of Gen Z say constantly learning interesting things would make them feel more engaged at work. They’re not the only ones. More than a third of workers in China and Brazil and over 10% in the U.S. and U.K. are learning additional skills because of economic worries.

Over a third of U.S. and U.K. workers also are more engaged with their bosses, and over 40% are taking on more responsibly because of recession fears. This is an opportunity for employers and managers who can provide useful feedback and growth opportunities.

Evolve With Shifting Consumer Preferences

Companies can’t afford to lose their best customers to competitors offering lower prices. Over a quarter of consumers are using more coupons, and almost half in the United States and United Kingdom are buying on sale because of inflation. Businesses need to identify which consumers are worth keeping and offer them the best value to retain their loyalty.

Companies also need to use the right technology to reach these consumers. About a third of U.S. and U.K. shoppers, and even higher percentages in China and Brazil, now comparison-shop online for bargains. That includes those 55 and older, who may have preferred to shop in-person before the pandemic.

Businesses also have an opportunity to attract new consumers or expand the products they provide to existing customers. For example, financial firms could offer services to consumers paying down credit card debt, increasing their savings and learning new budgeting skills because of inflation.

Automakers have an opportunity to tap into the growing demand for electric vehicles, especially if they offer access to free charging stations — the most valued incentive for customers right now, according to our survey data.

Businesses can’t wait for inflation to shrink and the economy to normalize. They must focus on what they can do — reduce risk and increase opportunity by creating plans, investing in employees and aligning with crucial customers.

This piece has been reprinted from the Oliver Wyman Forum.